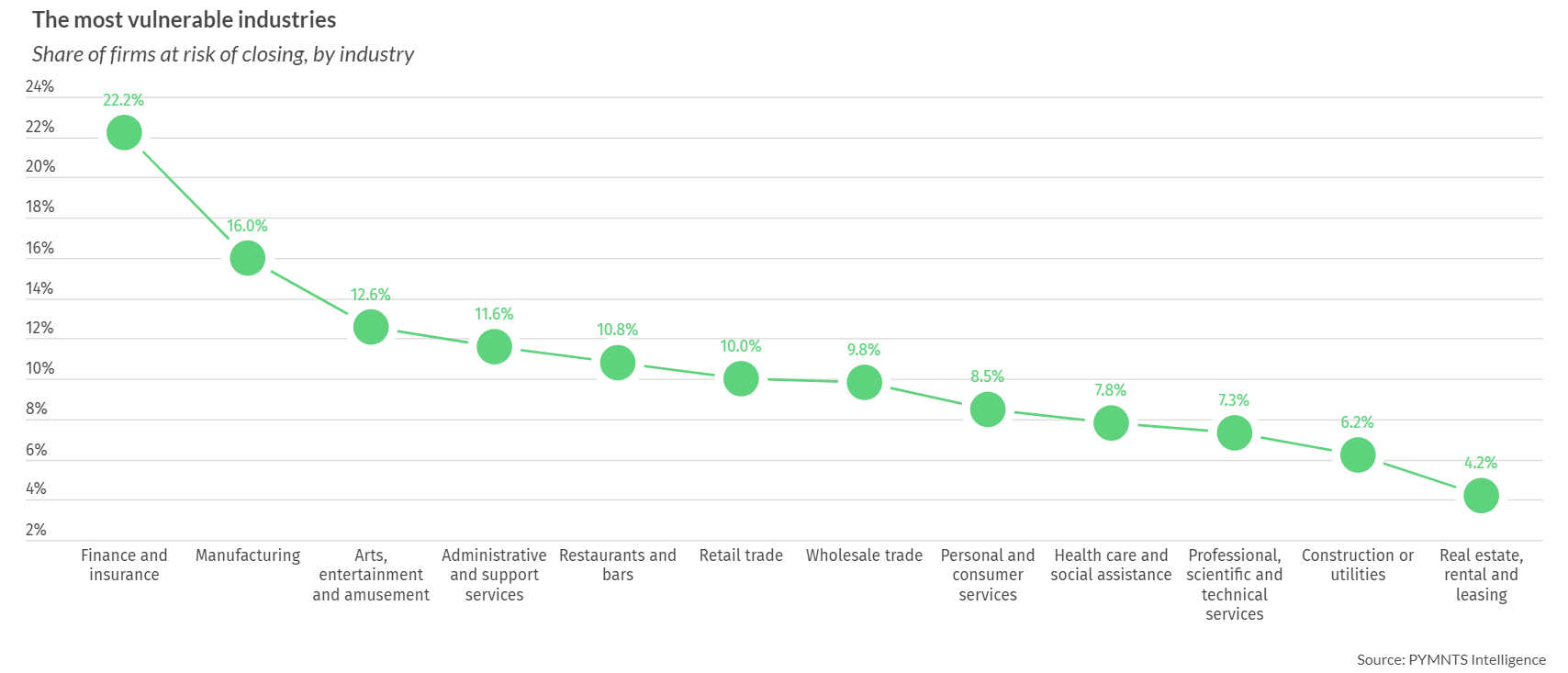

Finance denied to 400,000 small businesses over risk confusion: Report – StartupSmart

A new report reveals almost 400,000 small businesses are missing out on access to mainstream finance because credit providers are unable to adequately assess and price small business risk.

According to the Dun & Bradstreet report, which focuses on small business credit, there are more than one million unincorporated businesses in Australia.

Of these, the report reveals more than 650,000 have no major financial obligation and nearly 400,000 would immediately qualify for finance, with a risk profile ranging from minimal to low.

Dun & Bradstreet chief executive Gareth Jones says lenders have historically been hesitant about extending credit to small businesses because many of them are unincorporated entities with little or no commercial credit history.

“Previously, it has been nearly impossible to appropriately assess small business risk as small businesses are often indistinguishable from their owner – the commercial and consumer entity are the same,” Jones says.

“A holistic picture of small business risk can only be obtained by acquiring an understanding of an entity’s commercial and consumer profile.”

Dun & Bradstreet has created a Small Business Risk Score, which can predict the likelihood of a small business entering bankruptcy over a 12-month period.

The score considers a number of factors including business-to-business trade payment data, the time since the last consumer default, and the volume of credit enquiries.

The report comes on the back of fresh data from the Institute of Factors and Discounters, which shows debtor finance is becoming an increasingly popular funding source for small businesses.

IFD statistics for the December quarter show Australian debtor finance turnover was $16.3 billion – a 4% increase from the preceding quarter.

Meanwhile, turnover for the 12 months to December 2011 was $61.4 billion – up 4.6% from the 12 months ending December 2010.

By comparison, total business credit is rising more slowly than debtor finance, with Reserve Bank statistics showing business credit increased by just 1.4% over the year to January 2011.

Rod Lamers, head of debtor finance of Oxford Funding, says an increasing number of firms are looking for a more efficient way to manage their cashflow, hence the growth in debtor finance.

“Factors such as economic pressure from the continued strength of the Australian dollar, high wage costs and interest rates are putting strain on the cashflow of many businesses,” he says.

“Additionally, property assets are not increasing as much as they have historically, so alternatives such as debtor finance… become more viable.”

“Access to funding that scales with the growth of a business’s sales is especially appealing for businesses seeking this flexibility for seasonal fluctuations.”