How Australia compares to the rest of the world on cashless payments – StartupSmart

Ever since computers were first introduced into the retail banking system in the late 1950s, there has been the vision of a future world where cash is obsolete. The near death of personal cheques, increase in debit and credit card use, and innovations such as PayPal, Square, Apple Pay and Bitcoin, have led us to believe the cashless society is well within our reach.

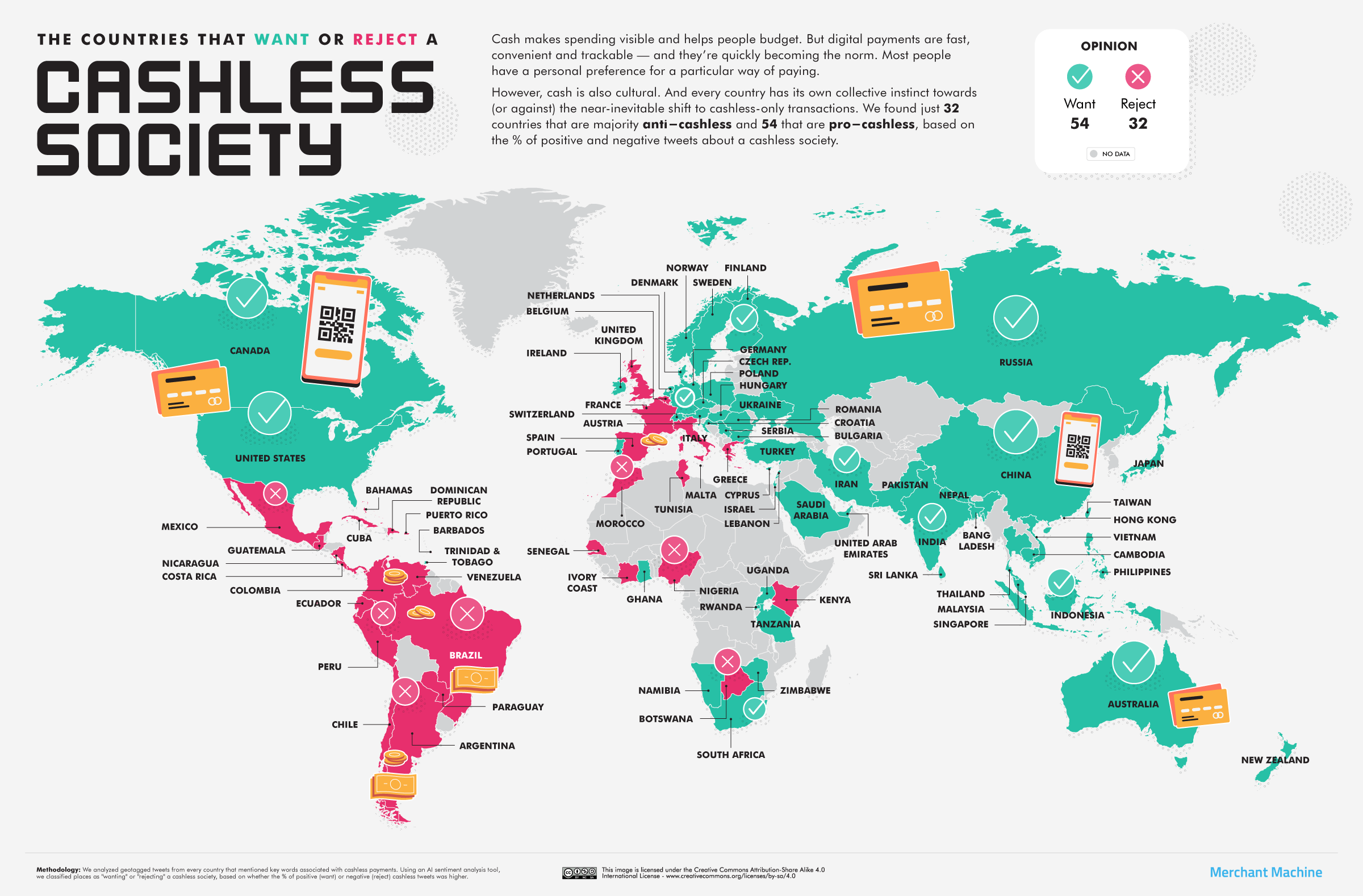

But data from Retail Banking Research, one of the most authoritative sources in the area, suggests that even though cashless payments are growing rapidly across the world, hard currency remains resilient. This trend was corroborated by a study commissioned by the ATM Industry Association of a panel of 13 countries. It suggested that global demand for cash grew 4.5% between 2009 and 2013 (when the latest figures were available).

So 50 years into the journey and we are still not there yet. However, a number of innovations have taken place around the world. Here’s how different continents stack up.

Europe

One in ten card payments were contactless for the first time in 2015 in the UK. By making small payments easier and quicker, contactless marks a major threat to cash. London is also fast becoming the world’s fintech capital, despite having substantially fewer resources available for investment than the US.

Next summer Copenhagen will host Money 20/20, the world’s major annual event for emerging payment technology. It will be the first time the forum convenes outside the US, bearing witness to the increasing importance of Europe when it comes to innovation in payments and financial technology. In countries like the Netherlands there are cafes and even supermarkets that no longer accept cash.

Many have pointed to the slow death of cash in Scandinavia, but cash is unlikely to completely die out – few may develop a mobile app suited to the needs of refugee migrants there, for example.

North America

Despite playing host to the world’s top technology firms and research centres, the US lags behind when it comes to implementing some of this tech. Chip and pin payment cards were only launched in October 2015 and do not seem to have done well over the Christmas holiday season, with reports of large retailers bypassing card readers and going back to signatures. This might seem backward but it’s important to remember that chip and pin cards are as much a protocol to determine who will bear the cost of fraud as a security feature.

And, while the US has been slow to introduce chip and pin, there have been developments in smartphone payments. The bank JP Morgan Chase and retailer Walmart have both launched rivals to Apple Pay, which shows how retailers, banks and regulators are innovating to bring about faster payments and a potential cashless society.

Africa and the Middle East

The success of the mobile payments system, M-Pesa, in increasing financial inclusion in Kenya is well known, with the majority of the population able to transfer money using their phones, despite not having a bank account. And there has been similar growth of mobile payments in Botswana and South Africa. But Safaricom (the telecom company behind M-Pesa) has failed to replicate its model in neighbouring countries such as Tanzania. The jury is also out regarding the Cash-less Nigeria Project by its central bank, which aims to reduce the the amount of physical cash circulating in the economy.

Africa and the Middle East remain the areas with the lowest global numbers of adults with a bank account while MENA countries (as well as China and other Asia Pacific nations) have been and will continue to be the worlds’ growth markets for ATM manufacturers. This suggests the high use of banknotes in the everyday life of people in these regions.

Asia, Latin America and Oceania

In China, the mobile app WeChat is one to watch. WeChat, part of digital behemoth Tencent, has grown from its original service as a messaging app in 2011 to include cab-hailing, food-ordering and money transfers. WeChat ranks as China’s most popular app with 650m users and is used to send both RMB and cryptocurrencies like Bitcoin between users.

Technology as a promoter of financial inclusion is the name of the game in poor economies where the bottom third of the population hardly have any access to the financial sector and mobile money is seen as the potential solution. Chile is a notable example of successful government initiatives in this direction. But the one to watch is the Indian government’s drive to replace money with mobile payments on top of a growing private network made up of 140,000 private business and public sector bank correspondents.

The challenge for mobile money, however, is that it sits at the intersection of finance and telecommunication and so faces regulations from both. On top of that, India and other countries in Asia and Latin America have a significant number of transactions that take place outside the formal financial sector and typically, an over-regulated telecommunications sector. At the same time, those at the “bottom of the pyramid” are fearful of and distrust established financial institutions.

Australia offers a much brighter outlook. The introduction of contactless payment cards in 2010 has proven hugely successful and as a result plastic has significantly eroded the use of cash and ATMs. Indeed, a recent study by the Reserve Bank of Australia found that the use of banknotes and coins fell from 69% in 2007 to just 47% in 2013. That decline took place across all age and income groups, with people in rural locations more likely to be using cash than those in major cities.

While some countries have embraced mostly electronic forms of payment, this does not mean that others still using banknotes and coins are less efficient or backward as some might seem to think. Differences between countries and between rich and poor within them remain partly due to custom, culture and regulation. But also because new technology has failed to make its case to users.

There is more innovative technology looking for a market than consumers looking for alternative ways to pay. And there is nothing wrong with existing forms of payment – they, and cash in particular, work well in most countries, for most consumers, 99% of the time. Of course, people change their habits and financial technology start-ups may one day disrupt the status quo.

Bernardo Batiz-Lazo, Professor of Business History and Bank Management, Bangor University; Leonidas Efthymiou, Lecturer in Management and Strategy, Intercollege Larnaca, and Sophia Michael, Languages Department Coordinator/Lecturer of English, Intercollege Larnaca

This article was originally published on The Conversation. Read the original article.