How to determine whether you qualify for the R&D Tax Incentive – StartupSmart

My business is innovative and experimenting with new ideas. How do I determine whether we qualify for the R&D Tax Incentive?

The Research and Development (R&D) Tax Incentive program was developed to assist businesses recover some of the costs of undertaking R&D.

The program is administered jointly by AusIndustry and the Tax Office. The R&D tax incentive provides a tax offset to eligible companies that engage in R&D activities.

Companies engaged in R&D may be eligible for either:

- a 45% refundable tax offset (equivalent to a 150% deduction) – for entities with an aggregated turnover of less than $20 million per annum, or

- a 40% non-refundable tax offset (equivalent to a 133% deduction) – for all other entities.

Eligibility begins with the structure that is conducting the R&D. The following are considered eligible entities:

- an Australian resident company; or

- a foreign company that:

- is a resident of a country with which Australia has a double tax agreement; and

- carries on R&D activities through a permanent establishment in Australia; or

- a public trading trust with a corporate trustee.

If you are operating through an eligible entity, you must register your R&D activities with AusIndustry:

- within 10 months after the end of the income year (registering for the income year in which the offset is to be claimed), and

- prior to claiming the R&D tax offset in the tax return.

This means that you have until 30 April to submit your R&D application with AusIndustry. Once you have met the deadline and submitted your application, AusIndustry will review your activities in order to determine whether they are eligible ‘core activities’.

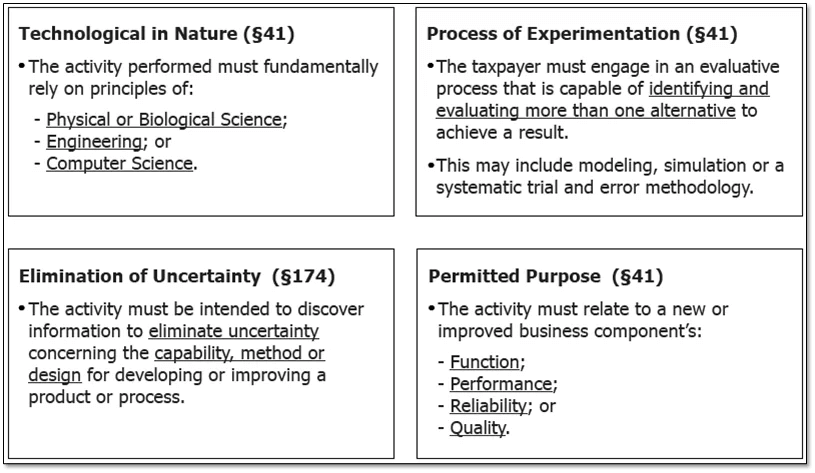

To be eligible, core activities must be experimental. Experimental activities are (as per the Tax Office’s Guide to the Research and development tax incentive):

- activities whose outcome cannot be known or determined in advance on the basis of current knowledge, information or experience, but can only be determined by applying a systematic progression of work that:

- is based on principles of established science; and

- proceeds from hypothesis to experiment, observation and evaluation, and leads to logical conclusions, and

- that are conducted for the purpose of generating new knowledge (including about creating new knowledge or improved materials, products, devices, processes or services).

Excluded activities can be found through the AusIndustry website.

Non-core R&D activities include:

- market research;

- management studies or efficiency surveys;

- developing, modifying or customising computer software for the dominant purpose of internal administration of business functions; and

- commercial, legal and administrative aspects of patenting, licensing or other activities.

The registration of R&D activities is managed by AusIndustry, which checks that the activities comply with the law. The Australian Tax Office (ATO) determines the eligibility of the expenditure claimed in the company tax return.

A common misconception is that the R&D Tax Incentive is a government grant.

It is a tax incentive and its benefits flow through the company tax return. This means that the R&D Tax Incentive has nothing to do with government grants.

The law and logic here is that anyone advising businesses on R&D Tax for a fee must be a registered tax agent. Make sure that your adviser is one and has the experience necessary to guide you. If in doubt, visit the Tax Practitioners Board website.

One final note – the deadline for the 2012/13 financial year for the submission of the R&D application and activity registration form is 30 April 2014. Best to connect with your tax advisor before the April rush.